Is it worth investing in European stock markets?

Eurozone equities have made strong gains in 2017. The eurozone stock market, as measured by the MSCI EMU index, has returned 11.9% in the year to 31 May.

Reduced political risk

A large part of the reason for Europe’s recent gains is that investors are less worried about political risk. At the start of the year, investors faced a calendar full of elections in countries including the Netherlands and France.

Many investors feared that these elections could see victories for anti-EU candidates, and possibly even lead to the break-up of the eurozone.

That scenario hasn’t come to pass. Eurozone equities enjoyed strong gains in the wake of the Dutch and French elections when centrist candidates were declared the victors.

Meanwhile, the forthcoming German elections are not expected to result in a radical change to existing government policy. Elections in Italy are due no later than May 2018.

Eurozone shares still attractively valued

Given the recent gains, it may be worth considering whether the eurozone stock market still represents good value.

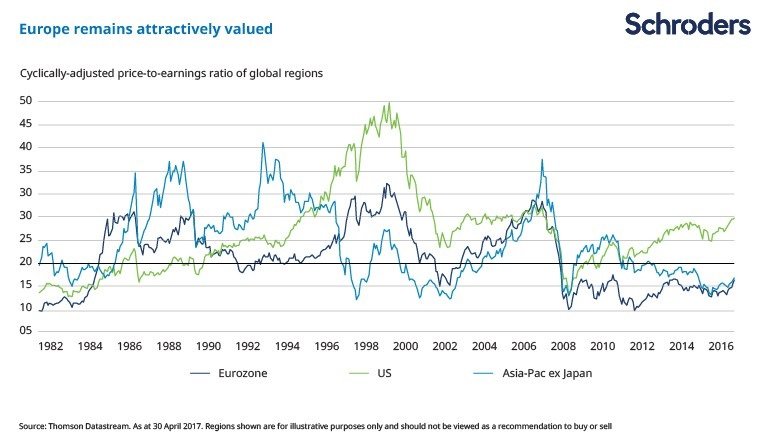

Investors can use a number of metrics to work out a stock market’s valuation. One frequently used measure is the cyclically-adjusted price-to-earnings ratio, or CAPE. This is defined as the share price divided by the average of ten years of earnings, adjusted for inflation. A lower figure suggests better value.

The chart below shows the CAPE valuation for the eurozone, US, and Asia ex Japan regions going back to 1982.

The eurozone’s current CAPE ratio of 15.6x is below its own long-term average of 19.9x, indicating it is currently lowly valued compared to its own history. It is also well below that of the US market and in line with Asia.

Earnings improvements could offer support

So, the eurozone stock market may appear to be attractively valued, but what can drive further gains from here? Some investors point to the region’s economic recovery which has been gathering momentum since summer 2016. There is also the prospect that corporate earnings could improve.

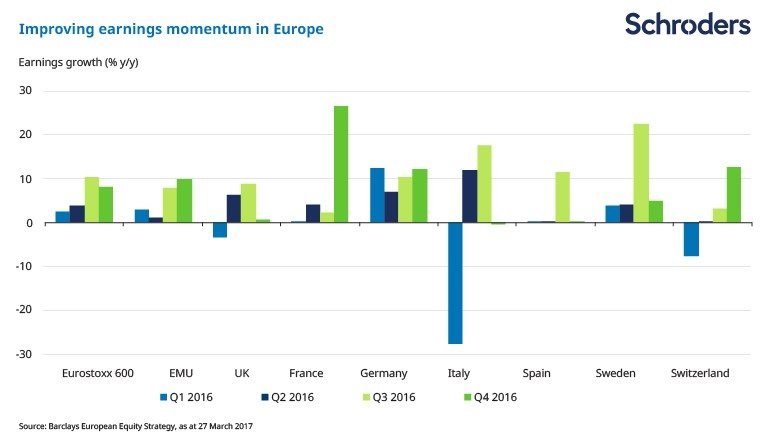

Corporate earnings growth in Europe has been lacklustre in recent years due to the slow economic recovery from the financial crisis. Ultra-low levels of inflation have made it difficult for companies to raise prices, which has in turn been a drag on profits.

However, recent earnings seasons have painted a more positive picture. The chart below shows that corporate earnings in Europe picked up significantly over the course of 2016.

View from a fund manager:

Nicholette MacDonald-Brown, portfolio manager and co-head of pan-European equity research at Schroders, said: “The outcome of recent eurozone elections should allow equity investors to concentrate on the broadening economic recovery, rather than fearing a potential break-up of the euro.

“Equity valuations are very attractive in Europe, both in an absolute and relative sense. If you combine this with the accelerating earnings growth we are currently seeing, then we think European equities could offer an attractive opportunity to investors. The recent earnings season has been very encouraging with sales and profits beats from a large number of companies across a variety of sectors.

“Recent European survey data indicates that the consumer recovery has been joined by a manufacturing one. As manufacturing confidence transforms into higher investment spending and higher levels of employment, this should in turn feed back into the consumer’s pocket. This would broaden the base of the economic recovery, boosting its stability. All of this would be good for equity markets.

“At current valuations, investors have the opportunity to take advantage of a strengthening and synchronised economic growth environment where the political risk is declining.”

Please remember that past performance is not a guide to future performance and may not be repeated. The value of investments and the income from them may go down as well as up and investors may not get back the amounts originally invested. Exchange rate changes may cause the value of any overseas investments to rise or fall.