This stock market index rose 289% but could still be good value

Over time, smaller company shares have outperformed larger ones, research shows.

The FTSE Small Cap index has risen 289% since its nadir in February 2009, compared with a 158% rise for the FTSE 100.

Because of their size, “small caps” have the potential to grow more quickly. The quicker a company can grow its earnings in a sustainable way the more attractive it is to investors.

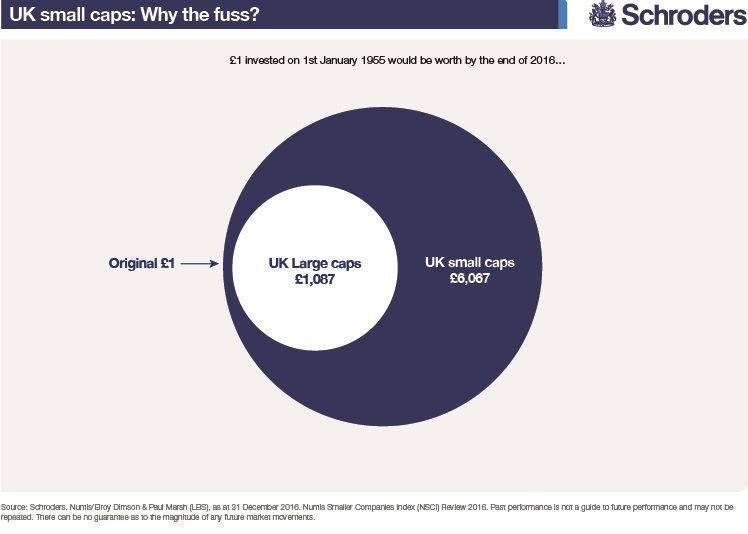

A recent study by broker Numis and the London Business School showed that UK smaller company shares have delivered better total returns than larger companies over more than 60 years.

The study found that one pound invested in UK large companies in 1955 with dividends reinvested would have grown to £1,087 by the end of 2016. That same pound put into small companies would have grown to £6,067.

Paul Marriage, Head of Dynamic Small Cap at Schroders, said: “You can think of small investing in the same way as parenting. When the companies are at a very early stage, they are problematic. Likewise, any parent will tell you the ‘terrible twos’ is a difficult time. And once companies get too big, they are then teenagers, becoming potentially hard to manage.

“But in between these two phases is potentially a sweet-spot for parents and investors alike. This is the stage at which we invest, after the toddler stage but before the teens.”

What is a small cap stock?

The definition of small cap can vary and moves over time, but generally the companies will be in the bottom 10% by size of the UK market at the time of purchase.

Examples of companies you might have heard of that started life as small caps and rapidly become large caps or larger well known midcaps, include food wholesaler Booker, which has just struck a merger deal with Tesco, and drinks firm Fever-Tree.

Are small caps still outperforming?

Few investors would have been lucky enough to have invested over the period of bumper returns from 1955. So how have small caps fared more recently?

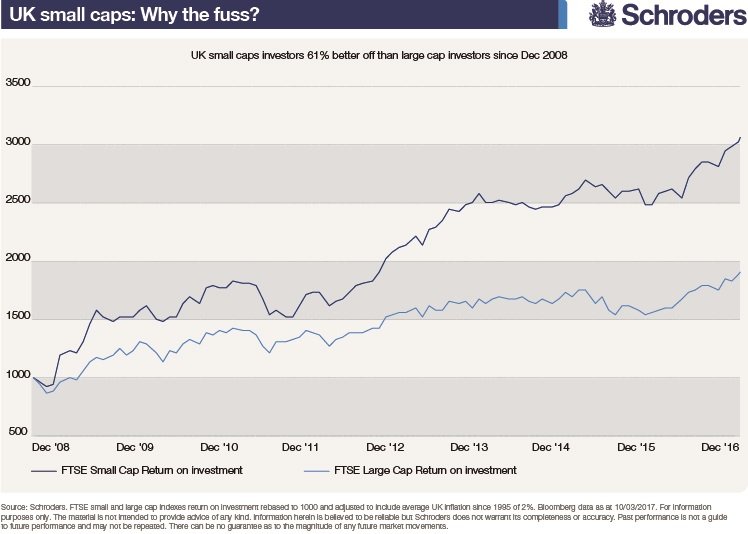

We looked at a shorter timeframe from the height of the financial crisis, when conditions were tougher than at any time in living memory for businesses, particularly smaller companies.

Still, UK small caps outperformed. The FTSE Small Cap index has returned 290%, including dividends, since the depths of the financial crisis in February 2009. In the same period the FTSE 100 returned 156%.

- This is why the FTSE 100 rises – explained in two charts

- After a 37% rise is it still worth investing in the FTSE 100?

If you invested £1,000 in the FTSE Small Cap index at the end of December 2008 your investment would now be worth £3,055, including all dividends reinvested and adjusted for the effects of inflation. If you put the same amount of money in the FTSE 100 your investment would now be worth £1,908.

Are small caps still worth buying?

Bumper gains may put off some potential investors, who might assume the strong rises have made small caps expensive. But we believe that some UK small caps remain good value relative to larger companies.

One way to value individual shares or the stockmarket as a whole is to compare share prices and earnings in a price-to-earnings ratio (P/E). A lower P/E ratio suggests better value.

Since 2007, the average median P/E of the FTSE 100 has been 11.6, and FTSE Small Cap index has been 11.1; so on average small caps have traded at a 4.5% discount to large cap.

Currently, that discount is wider at 12.5% with the FTSE 100 on 14.5 versus FTSE Small Cap index on 12.7.

Why consider small caps?

Stephanie Madgett, Schroders' Small Cap Equity Analyst, said:

“There are more opportunities to find investments with material upside within small caps.

“Due to their size they are less well covered by analysts and the media, so investors tend not to be as aware of them.

“Once a small cap company starts to deliver you could potentially get a double whammy effect of growth and rerating. A small cap stock might go from a P/E of 10 to 20 times once it starts to grow and get discovered.

“That is much more difficult to achieve with larger companies.”

Four ingredients for a successful small cap investment:

- The company should be a market leader in its niche.

- The company should have a unique product or service to differentiate it from rivals.

- The company should have good management who hold substantial stakes in the business. (i.e. owning more than 5% of share capital).

- The company should be cash generative and profitable.

Please note that past performance is not a guide to future performance and may not be repeated. The value of investments and the income from them may go down as well as up and investors may not get back the amounts originally invested.

- Read more at Schroders.com and follow us on twitter

Important Information: The views and opinions contained herein are those of David Brett, Investment Writer, and may not necessarily represent views expressed or reflected in other Schroders communications, strategies or funds. The sectors and securities shown above are for illustrative purposes only and are not to be considered a recommendation to buy or sell. This material is intended to be for information purposes only and is not intended as promotional material in any respect. The material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. The material is not intended to provide and should not be relied on for accounting, legal or tax advice, or investment recommendations. Reliance should not be placed on the views and information in this document when taking individual investment and/or strategic decisions. Past performance is not a guide to future performance and may not be repeated. The value of investments and the income from them may go down as well as up and investors may not get back the amounts originally invested. All investments involve risks including the risk of possible loss of principal. Information herein is believed to be reliable but Schroders does not warrant its completeness or accuracy. Reliance should not be placed on the views and information in this document when taking individual investment and/or strategic decisions. The opinions in this document include some forecasted views. We believe we are basing our expectations and beliefs on reasonable assumptions within the bounds of what we currently know. However, there is no guarantee than any forecasts or opinions will be realised. These views and opinions may change. Issued by Schroder Investment Management Limited, 31 Gresham Street, London EC2V 7QA. Registration No. 1893220 England. Authorised and regulated by the Financial Conduct Authority.