Two charts for those already suggesting the value bounce is finished

When you sign up to be a value investor, you soon learn you have not chosen the easiest path to tread. Even so, here on The Value Perspective, we still find ourselves occasionally astonished at the way the wider market can seem so willing to write off the discipline’s prospects. Take the recent resurgence in value – it has been going for all of three months and already there are suggestions in some quarters it is over.

So, we might be forgiven for asking, growth pulls off the historically anomalous trick of outperforming value for the last nine years, give or take, and nobody seems too bothered? And yet, just a few months into this small uptick in value’s fortunes versus growth, its ‘That’s all, folks. If you aren’t invested by now, sorry but you’ve missed the boat. Move on – nothing to see here’? Seriously?

Let’s get a disclaimer in quickly. What we are about to say in no way implies a belief that, if you buy into value, from this point in time you are going to make a mint. Value is at present, we believe, moderately priced versus history. But take a look at the two charts we have to show you and decide for yourself whether the last few months have seen any real kind of equilibrium restored between value and growth.

- Receive views on value investing: The Value Perspective Newsletter

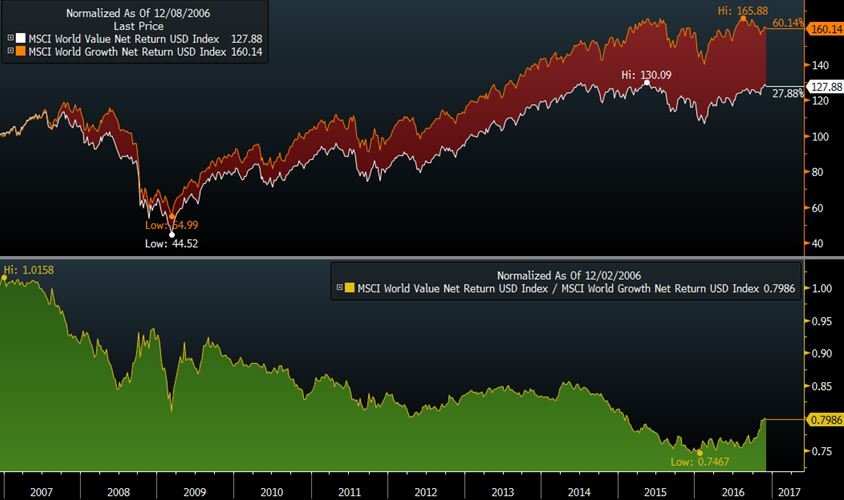

The first chart shows the relative performance of the value and growth strains of the MSCI World index and two things are immediately apparent. First, as we said, value has had a pretty torrid time of it since 2007 and, second, the great performance it has enjoyed over the last few months registers as the slightest of reversals of fortune in what has been a very tough decade.

MSCI World index – value v growth

Source: Bloomberg, data shown from 2 December 2006 to 29 November 2016. Past performance is not a guide to future performance and may not be repeated

Now, whether you are looking at multiples of price to tangible book value, price-to-sales, bottoms-on-seats or whatever metric you prefer, a sensible way to consider the valuation of a sector or, in this case, investment style, is to think about what you are paying for the actual physical assets of the underlying businesses – which brings us to our second chart.

Source: Schroders, Thomson Datastream, data shown from 31 December 1997 to 29 November 2016

The valuation metric we have chosen is price to tangible book value and, while the ups and downs of the value line are not as pronounced as they might be – we felt it was important to show it on the same graph as the growth line – you should still be able to make out that MSCI World index businesses classified as value saw their valuations fall around the time of the financial crisis. They have not really recovered since.

- More value investing ideas on Twitter: @Thevalueteam

- Find out more: What is value investing?

Rather more apparent is the dramatic rise in the multiples investors have been willing to pay for growth over the last four years or so – even greater, it is worth noting, than at the height of the technology bubble in 1999/2000. This has played a very significant part in value’s dramatic underperformance versus growth and while, yes, the situation has reversed a little in recent years, those growth multiples are still very elevated.

That is why we hope you will forgive us if we roll our eyes each time we are told the value ship has already sailed. No, we are not suggesting value, from here, represents a one-way ticket to untold riches – as we said at the start, value now stands moderately priced versus history. By the same token, however, growth is hugely overpriced and the chances of it losing investors money from this point are similar great.

Important Information: The views and opinions contained herein are those of Ian Kelly, Fund Manager, and may not necessarily represent views expressed or reflected in other Schroders communications, strategies or funds. The sectors and securities shown above are for illustrative purposes only and are not to be considered a recommendation to buy or sell. This material is intended to be for information purposes only and is not intended as promotional material in any respect. The material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. The material is not intended to provide and should not be relied on for accounting, legal or tax advice, or investment recommendations. Reliance should not be placed on the views and information in this document when taking individual investment and/or strategic decisions. Past performance is not a guide to future performance and may not be repeated. The value of investments and the income from them may go down as well as up and investors may not get back the amounts originally invested. All investments involve risks including the risk of possible loss of principal. Information herein is believed to be reliable but Schroders does not warrant its completeness or accuracy. Reliance should not be placed on the views and information in this document when taking individual investment and/or strategic decisions. The opinions in this document include some forecasted views. We believe we are basing our expectations and beliefs on reasonable assumptions within the bounds of what we currently know. However, there is no guarantee than any forecasts or opinions will be realised. These views and opinions may change. Issued by Schroder Investment Management Limited, 31 Gresham Street, London EC2V 7QA. Registration No. 1893220 England. Authorised and regulated by the Financial Conduct Authority.