House prices near Crossrail stations have risen as much as 82 per cent since it was announced

House prices within a 10 minute walk of Bond Street station have risen 82 per cent since Crossrail was first announced in 2008, a report published this morning suggested – almost twice the 43 per cent rise experienced in the wider area.

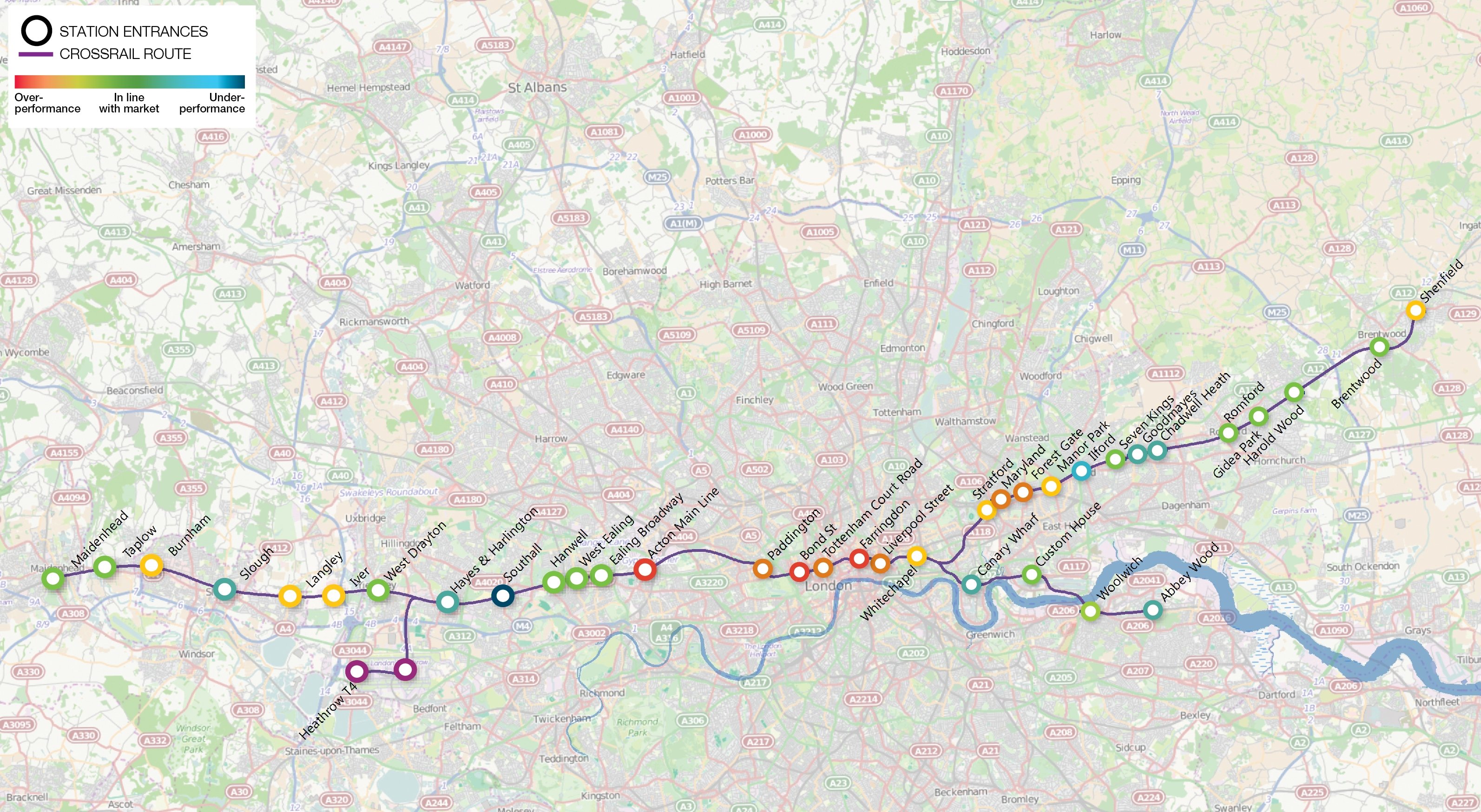

Bond Street isn't the only over-performing Crossrail site, though: according to Knight Frank's Crossrail report, prices around Acton have risen 77 per cent since the line was first announced, while Farringdon has jumped 24 per cent.

Click or tap to open in a new window.

Source: Knight Frank

The report also highlighted areas that have underperformed, relative to expectations. Investors looking for a place to stash their cash could do worse than looking at properties around Southall, Hayes & Harlington and Slough to the west of London, and Manor Park, Goodmayes and Chadwell Heath to the east.

However, the report suggested average residential price growth around stations along the Crossrail route have outperformed local areas by five per cent.

It is worth noting that these stations have undergone, or are undergoing, serious re-development, with an overhaul of the public realm surrounding them, underlining the part played by regeneration in underpinning property price growth.

The route, which at £14.8bn is one of the most expensive infrastructure projects undertaken in recent times, is due to come into service in 2018, with the final phases being completed in late 2019.

Gráinne Gilmore, Knight Frank's head of UK residential research, said Crossrail had started a "ripple effect".

Our research shows overall price performance continues to be stronger in the central London sections of the Crossrail route. However, over the last 12 months, the price ‘ripple’ effect in London has really started to take effect, with stronger price growth in areas surrounding central London. This could help feed into stronger price growth around stations towards the east and west, especially those which have underperformed to date, and where housing supply is set to be delivered in the coming years.