Quantitative easing is go – but euro plummets as European Central Bank unveils €60bn-a-month bond buying programme

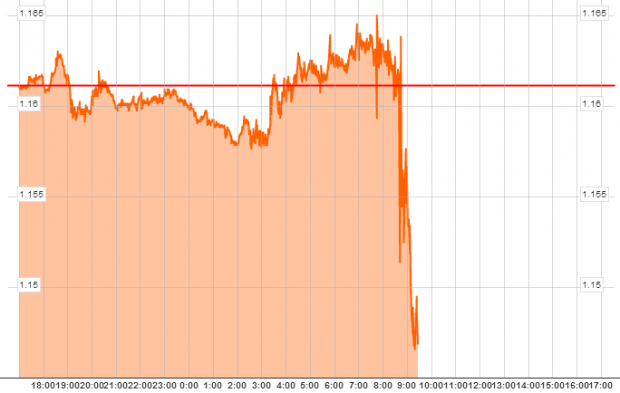

The euro has fallen sharply, dropping 1.2 per cent to 1.1475 against the dollar, its lowest in 11 years, and 1.02 per cent to 0.7589 against the pound after European Central Bank (ECB) president Mario Draghi announced a €60bn-a-month government bond-buying programme – much higher than the expected €50bn a month.

A little out of breath because of broken-down lifts, Draghi said this afternoon that the programme will last at least until the end of September 2016 – meaning the programme will total €1.26 trillion euros.

With its main interest rate at just 0.05 per cent (which the bank voted to hold today), Draghi had a limited arsenal of weapons to counter inflationary pressures, after the Eurozone slipped into deflation in December for the first time since 2009, with a 0.2 per cent year-on-year fall in prices.

QE – his so-called "last bazooka" – was a final resort, but does give the ECB more control over the bloc's prices.

The euro fell sharply against the dollar (Source: Bloomberg)

As recently as the beginning of this month, there had been speculation the bank would avoid a fully-fledged QE programme altogether. But last week a decision by the European Court of Justice effectively gave it the green light, when it ruled a previous monetary easing policy, called Outright Monetary Transactions (OMT), was "compatible in principle" with European law.

The ruling was in response to a legal challenge by the Germans – and it's likely Angela Merkel et al are still unhappy with today's decision by the ECB. Within minutes of Draghi's announcement, deputy chancellor Hans Michelbach asserted that the ECB was "violating its mandate".

However, at a session at the World Economic Forum in Davos this morning, legendary economist Larry Summers suggested investors had already priced this round of QE into their transactions, meaning its impact could end up being weaker than expected.

We’ve already had a set of positive developments, and the economic forecasts are pretty dismal from here“I am all for European QE, but the risks of doing too little far exceed the risks of doing too much. Deflation and secular stagnation are the macro-economic threat of our time. That said, I think it is a mistake to suppose QE is a panacea or that it will be sufficient. We’re all for QE in Europe. We can’t afford not to have it. It’s necessary, but it’s not sufficient.

Darren Hepworth, global

Others have warned that politicians cannot use the programme to "avoid tough decisions". James Sproule, the Institute of Directors' chief economist, said:

Ultimately, QE on its own risks setting the Eurozone on the road to Japanese-style stagnation and deflation. QE is not, should not and cannot be seen as a substitute for the kind of structural reforms to labour and product markets that the EU so desperately needs.