Euro periphery fails to rebalance and cut debts

SIX YEARS after the financial crisis struck, the disparate and struggling Eurozone economies have still not overcome their imbalances – and progress could be grinding to a halt, Standard and Poor’s analysts said yesterday.

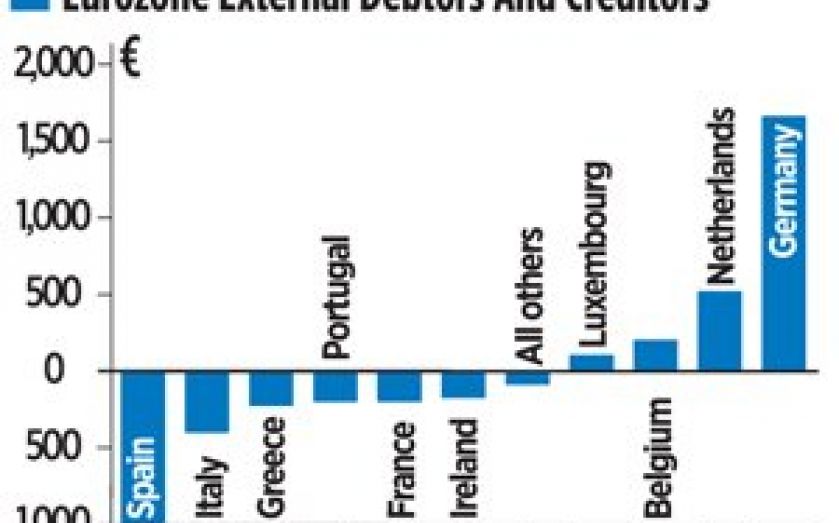

Despite their debt crises, the peripheral economies’ external debts have been growing.

Simultaneously, Germany and other strong nations have been increasing their loans to the countries – worsening, rather than improving the imbalances.

The peripheral nations have been through tough reforms, cutting public spending and freeing up their economies. But although further work is needed, S&P believes the momentum for reform is slowing.

Analysts estimate Spain, Italy, Greece, and Portugal now owe a total of €1.85 trillion (£1.47 trillion) to foreigners, up from €875bn in 2004.

Over the same time period, Germany, the Netherlands and Belgium have seen their net external asset position grow from €343bn to €2.36 trillion.

Standard and Poor’s expects this to hurt growth for years to come.

“The blocked channel of internal Eurozone adjustment could further draw out the desired external deleveraging in the debtor countries, extending the period of weak demand and growth in those economies,” its report said.

Meanwhile, inflation is set to fall lower – another sign of stagnation in the currency area. Market expectations of average inflation over the coming five years have slipped to a record low, of below 1.7 per cent. Countries such as Greece are already suffering outright deflation.