Sluggish wage growth gives Bank of England a tough choice over interest rates

Unemployment rate: down. Wages: up a tiny bit.

How does this affect the Bank of England's plans for interest rates? At six per cent, according to the Office of National Statistics (ONS), the unemployment rate is looking healthier by the month.

It’s comparable to the US rate (5.9 per cent) and far lower than our neighbours across the channel. France, for example, has a rate of 10.6 per cent and the Eurozone as a whole is running at 10.1 per cent.

The latest US data actually showed 5.9 per cent in September, this is August's rate. UK rate is a three-month average.

All good, but wages are still struggling. Incremental rises in pay, below inflation (1.2 per cent), could affect the Bank of England's position on an interest rate hike.

The Bank has a mandate to keep inflation at two per cent, and anything above that would put more pressure on the monetary policy committee to raise rates. A lower inflation rate means pressure not to raise them from their historic low of 0.5 per cent.

Low wage growth also adds pressure on the Bank to keep rates low.

Creeping upward

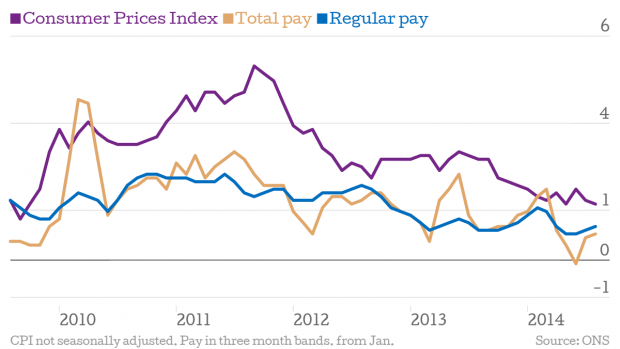

Pay including bonuses was up 0.7 per cent compared to a year earlier while pay including bonuses was up 0.9 per cent. This chart compares that growth to that of inflation:

These figures are arrived at by surveys rather than data from everyone in work, so any one figure may be inaccurate. The overall trend though isn’t going upwards at anywhere near the rate the Bank of England would like.

Mark Carney has indicated that he expects interest rates to rise before wages catch up with inflation, but continued sluggish wage growth and falling inflation may affect the timing of a hike.

Unemployment is key to any decision, but it is far from being the only factor, as Jonathan Pryor of Investec explains:

The six-year low in unemployment is likely to put the Monetary Policy Committee in a quandary about when to hike interest rates.Mark Carney made the unemployment rate a much publicised key barometer of when to hike rates but the unforeseen drop in consumer inflation and stalling wage inflation has put the Bank of England between a rock and a hard place.For now it appears that investors believe the first rate hike will come much later than the initial forecast of February and due to this the pound remains under pressure this morning, at almost twelve-month lows against USD.

In a speech earlier in the year, Carney had said a rate rise in the spring would be seen as the bank completing its mandate, but with no inflationary pressure to act, dawdling wage growth and signs the upward pressure on house prices is easing it may come later.