Value stocks: A canny investor’s choice

There is a long-running tug of war between two styles of investing: value and growth. The former sees investors select stocks with an intrinsic value. The definition varies, but tends to focus on companies with lower valuations and higher dividend yields. Growth investing is when investors tend to select stocks with growth potential, with valuation a secondary factor.

But why is this relevant now? The history of this debate has taught us that the period before an interest rate rise is when investors should be targeting value, not growth. And with a first Bank of England interest rate rise possible before the end of the year, investors should ensure that their portfolios are weighted towards traditional value industries such as energy, mining, financials and healthcare.

LIFTING ALL SHIPS

In an ever-improving global economic climate, it might seem counterintuitive to turn your focus away from growth stocks, but we see a compelling and logical reason for looking elsewhere. When the recovery becomes more broad-based, headline growth is likely to help the majority of companies. As a result, there is no need to pay a premium for a growth stock, when you can get equally good returns from value companies, which also usually trade more cheaply.

Indeed, much of the investor community is currently focused on UK mid-caps. But given the 10 per cent valuation premium of the FTSE 250 index, and its high exposure to interest rate sensitive sectors, investors would be better off turning to value. With a period of interest rate rises approaching in the coming months, certain sectors which mid-caps are heavily exposed to could well suffer.

And while the recent strength of the British pound has been tough on companies with high overseas earnings, the relative strength of the currency will lessen somewhat. With this in mind, we expect it to be less of a headwind for value companies. Further, the MSCI UK Value index trades at a 15 per cent discount to the UK market, which is in line with its long-term average.

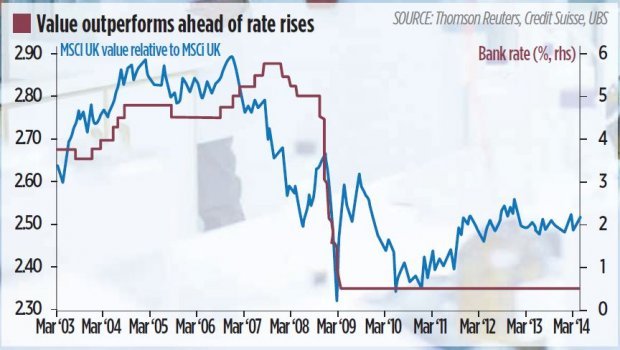

Consider the graph above. It shows the MSCI UK Value index’s relative performance against the UK market, plotted against UK bank base rates. There is a clear pattern that, as base rates fall, value underperforms. However, the overall trend is also that value outperforms in periods before rising base rates, as we are seeing now.

THE EFFECT OF M&A

The sharp increase in M&A activity this year is another major factor why investors should now target value stock investments. While M&A is traditionally the realm of mid-cap companies, in recent weeks we have seen a significant pick up in large-cap M&A in the healthcare and energy sectors. They both sit in the value index.

Further, with a broadening out of earnings growth, we believe investors will start to resent paying for high-growth stocks when they can now also gain earnings growth from value stocks, but at cheaper valuations. At UBS Wealth Management, we believe that value is under-owned and could benefit from continued market rotation as well as potential M&A. Many of the sectors in the value index are seeing substantial volumes of restructuring and thus offer more potential for M&A.

DELVING INTO THE DETAIL

Looking at the value sector in a little more detail, we are strong overweight on financials, as they tend to have strong links to our improving domestic economy, and generally many of the necessary adjustments have already been made. Healthcare, meanwhile, should be boosted by more M&A activity and restructuring as companies reposition for the next leg of growth – 2015 is expected to be the first year for some time that the healthcare sector posts positive earnings growth. Finally, we feel the worst is behind materials, as companies in the sector are starting to generate attractive positive cash flow.

The elephant in the room from a commodity pricing perspective is, of course, China. The key unknown concerns the impact of Chinese growth. If China continues to slow, and the long term picture suggests the brakes are firmly on, then it could impact commodity pricing unless the People’s Bank of China unveils large scale infrastructure stimulus packages to try and counter ailing growth.

Those readers who study the markets closely will justifiably point out that value stocks have slightly underperformed the wider market over the past two months. Concerns about global growth sent investors to seek the reliability of earnings from growth stocks, causing an underperformance of value during May. However, we believe that the recovery remains on track and that investors will return to the value style, as indeed they have already started to do in the past month, seeking good returns at more attractive valuations. Canny investors will spend the summer break reweighting their portfolios towards value before the first of the interest rate rises hits.

Caroline Simmons is deputy head of UK chief investment office at UBS Wealth Management UK.