Bretton Woods: How stable monetary order was created and then destroyed

NEXT month, financial history enthusiasts will commemorate the seventieth anniversary of the Bretton Woods Agreement.

In the 1940s, Bretton Woods was a somewhat faded New Hampshire resort town, but it is now forever associated with the three-week conference held there between 1 and 22 July 1944. The conference’s purpose was to set out a new monetary and financial order for a world torn apart by global conflict, and the subsequent agreement was a highly successful example of international cooperation. Countries engaged in a life or death struggle with the Axis powers were used to working together to come up with common solutions.

There has been nothing like it since. Today, the global economy lurches forward, seemingly without any plan or international initiatives. But what made Bretton Woods so important?

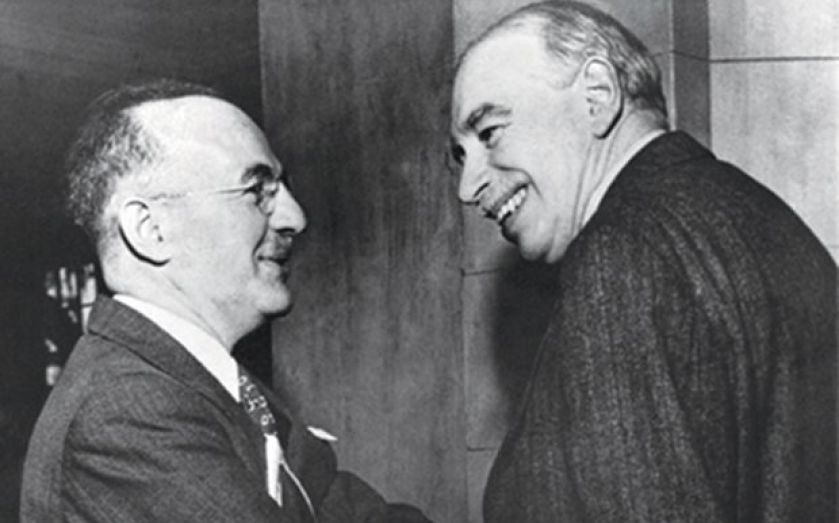

The proceedings in 1944 were dominated by John Maynard Keynes, the eminent British economist, and Harry Dexter White, the son of Lithuanian immigrants to the US. Keynes, the most famous economist in the world, was at first slightly dismissive of the prospect of an international gathering. Characteristically, he described Bretton Woods as the “most monstrous monkey house assembled for years”.

There were delegates from 44 countries mingling at the hotel, and Keynes thought that “acute alcohol poisoning would set in before the end”. Despite the prospect of endless committee meetings, major international political rivalries and copious amounts of drinking, the conference was effective. It helped to establish the World Bank and the IMF, both set up in Washington, DC.

Most significantly, from the point of view of international currency stability, Bretton Woods set the official price of gold at $35 per ounce. This value was, in effect, a continuation of the gold standard. As Bob Boothby, a Conservative MP, objected, “this is the gold standard all over again”. Of course, he was right.

But pegging the dollar to gold relied on prudent US economic management, basically keeping a balanced budget and not running big trade deficits. By the 1960s, however, the US public finances were under strain. US governments indulged in deficit spending to finance both the Vietnam War and an expanded social security system, the “Great Society” of Lyndon Johnson’s imagination. The Federal government believed it could pay for both guns and butter. This only led to more borrowing.

By 1971, the game was up. President Nixon unilaterally abandoned the fixed dollar price of gold established at Bretton Woods. Arthur Burns, then chairman of the Federal Reserve, argued passionately against its end. For the first time in a century, the dollar could not be converted to gold at a fixed price. Nixon himself believed gold to be a “monetary anachronism”. He was bored by international money. “I do not want to be bothered with international monetary matters”, he said. Critics saw Nixon’s move as an abandonment of the post-war liberal ideal of harmonious international trade. They saw Nixon’s shutting of the “gold window” as a return to US economic nationalism and the policy of “America First”.

The move away from a gold-backed dollar to a system of floating exchange rates seemed to many a fitting symbol of the decline of US power. The floating rate system that followed is still with us. Former German Chancellor Helmut Schmidt once called this a “floating non-system”.

A period of relative monetary order, between 1945 and 1971, has been followed by one of relative chaos. To one recent commentator, the abandonment of dollar convertibility into gold in 1971 marked the beginning of the process which led to an almost limitless expansion of credit, based on paper money. Many writers have observed the connection between paper money and sharp increases in all kinds of debt. One has even written “it is no coincidence that debt levels have exploded in the last forty years, culminating in the credit crisis of 2007 and 2008.”

It has been striking that no conference of the scale and ambition of Bretton Woods has been staged since 2008. G20 – a group of finance ministers and central bank governors from 20 major economies – has failed to become a significant forum for the development of international economic policy.

Beyond the practical difficulties of cooperation, it is also uncertain what kind of financial architecture countries want to see. There is no leadership or strategy with regard to trying to create a stable international monetary framework. Perhaps we don’t need one. But if “masterful inactivity” is the plan, we should at least have a discussion about whether this is really the best course to follow.

Kwasi Kwarteng is Conservative MP for Spelthorne, and author of War & Gold – A five hundred-year history of empires, adventures and debt (Bloomsbury, May 2014).